Are we giving the Federal Government too much Credit?

Federal debt has reached historic levels. It's history we should not be repeating. Do our politicians have Attention To Deficit Disorder?

WASHINGTON DC— What if you had a credit card that never maxed out? When you reached the credit limit you could increase it yourself, regardless of how much you overspent, and someone else paid the bill so that you could keep on spending as much as you wanted. In that case you’d likely be a member of the US Congress, or the President of the United States.

Last Monday the US Government surpassed what would have been—only a decade ago—an unimaginable milestone, or more aptly, millstone. The debt incurred by the federal government now exceeds $35 TRILLION. That’s 35 THOUSAND billion, or 35 MILLION million! It’s a truly staggering amount. To put this amount of debt in perspective, if you confiscated every penny from every millionaire in America—there are an estimated 22 millionaires in the US—you still couldn’t pay down the federal debt. The government now owes more than $100,000 for each American adult and child.

“America’s gross national debt topped $35 trillion for the first time on Monday,” reported the New York Times, “a reminder of the nation’s grim fiscal predicament as legislative fights over taxes and spending initiatives loom in Washington.” Gross indeed.

Meanwhile, Rome burns as politicians fiddle with whether or not Kamala Harris is really “black,” whether she was—or was not—the “border czar,” or whether JD Vance is really as crazy as he seems. “The leading presidential candidates, Vice President Kamala Harris and former President Donald J. Trump,” said the New York Times, “have said little about the nation’s deficits on the campaign trail, suggesting that the economic problem will only worsen in the coming years.”

Many of us might wish for more bipartisanship in Washington—seems every year there is less—but when it comes to spending money the federal government doesn’t have, Congress and the President have been dangerously bipartisan. Both Democratic and Republican Presidents, and Democrats and Republicans in Congress, have operated on continuous overdraft, writing checks with money they don't have but knowing won't bounce.

Maybe the reason you're not hearing much about the federal debt is that neither former president Trump nor Vice President Harris can credibly point the finger at the other, without having the same one pointed back at them. “In the presidential race, there’s not much partisan difference or advantage on this subject. Donald Trump and President Biden have overseen similar additions to the nation’s accumulated debt—in the range of $7 trillion in each case—during their terms,” says Gerald F. Seib, the Wall Street Journal’s former Executive Washington editor, “The national response to both has been, by and large, to look the other way.”

Only five years in the past sixty has the federal government run a surplus. The vast majority of the time it has run deficits—often massive ones that exceeded, sometimes far exceeded, 20% of the total budget. How is that level of financial irresponsibility sustainable? The answer, it’s probably not.

Saddled with more than $35 trillion of debt, the federal government now pays more in interest on debt than it does to defend the nation. “Net interest is the fastest growing category of federal spending,” a recent Washington Post editorial lamented. “For the first time ever, interest costs will exceed defense spending this fiscal year.”

Yet neither party seems all that eager to curtail spending, or to address runaway debt, with anything more than a press release. “Both political parties are using the debt mostly as a rationale for doing things they would like to do anyway,” according to Seib, “some Republicans to oppose more aid for Ukraine, for example, and some Democrats to raise taxes on corporations and the wealthy.”

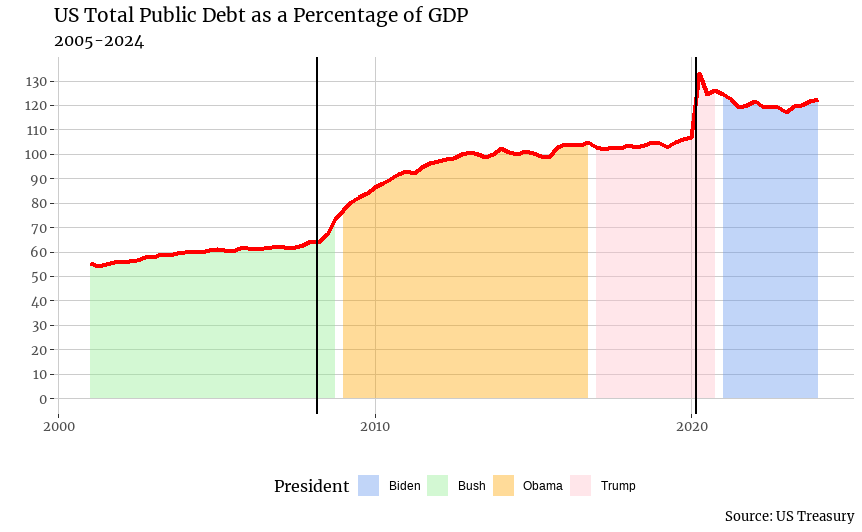

In addition to dollars, federal debt is often measured as a percentage of GDP, Gross Domestic Product, which is the total of all the goods and services produced by the US economy—everything that’s made, bought and sold. It’s also referred to as the total national output. “While income is usually measured in money,” according to economist and Senior Fellow at Stanford University, Thomas Sowell, “real income is measured in what money can buy, how much goods and services. The total real income of everyone in the national economy and the total national output are one and the same thing.”

“Only a dozen years ago, the aggregate government debt amounted to about 70% of the nation’s gross domestic product,” Seib said in his Wall Street Journal Guest Essay, “This red ink can have painful, if hidden, consequences. The CBO [Congressional Budget Office] projects that the weight of the debt will reduce income growth by 12% over the next three decades, as debt payments crowd out other investments.”

Attention To Deficit Disorder

Deficit spending isn’t necessarily a bad thing. It can be a useful tool to spur the economy or respond to catastrophic events. But like most tools, it’s designed for a specific purpose. You don’t use a screwdriver to drive a nail, at least you shouldn't—and politicians shouldn’t be using deficit spending as a way pay for things they want now, but can’t pay for now—or maybe ever.

Like a compulsive shopper, Washington politicians are addicted to spending, and not so much to paying. If you’re in Congress long enough, or you’re the President, it’s only a matter of time, it seems, before you contract “Attention To Deficit Disorder,” a political malady whose symptoms include no longer paying attention to budget deficits and sticking the bill to the American taxpayer.

So, if Congress and the President routinely ignore budget deficits, do deficits even matter?

Some economists, like Stephanie Kelton, a professor of economics and public policy at Stony Brook University, an advisor to US Senator Bernie Sanders, a favorite of Alexandria Ocasio-Cortez, and a proponent of Modern Monetary Theory (MMT), don’t think so. They don’t even think we should be using the term “deficit.”

“It would be far better, in my view, to simply call the resulting difference ‘net spending’,” she said. Kelton believes it’s not a deficit at all, since the government can print the money that makes up the difference between what it spends and what it receives in taxes. The federal government is, to MMT adherents, essentially an unlimited cash machine that can, and should, be accessed anytime (which is pretty much all the time) that the federal government runs out of money.

Kelton describes what you and I would call a “deficit” as how “much income the government is adding to the financial positions of the non-government sector.” The emphasis is hers, and it sounds like something unintelligible an economist might say. Since the government prints it’s own money it’s not “borrowing,” according to Kelton. “Ask yourself, does a currency-issuing government ever need to borrow its own currency from anyone?” Fortunately Kelton is very much in the economics minority.

Why the deficit should be of interest

“If we just have the debt keep growing, we have to pay interest on that,” Betsey Stevenson, a professor of economics and public policy at the University of Michigan said. “So we have to spend more ... just to pay the interest on the debt, which means that more of our budget needs to go towards the interest on the debt.” That means less for defense, social programs and infrastructure. And more debt can mean higher interest rates. The US is now actually borrowing to pay interest on the money the federal government has already borrowed.

One way the US pays for budget deficits is by selling bonds to investors, including institutional investors like hedge funds and banks. Increasingly, however, those “investors” include foreign nations like China. It’s estimated that foreign investors, including foreign governments, now “own” 40% of US debt.

Does it matter who “owns” US debt? As it turns out it very well might. Way back in 2007 the Brookings Institution, a Washington think-tank, issued a report that warned that “the United States continued dependence on foreign borrowing is a significant vulnerability in the event of shock, such as a collapse in U.S. housing prices, or an extreme national security breach, that might slow the inflow of new funds into the United States.” Again—this was when government debt was just a fraction of what it is today. Luckily, we haven’t had a catastrophe that would trigger that vulnerability—but it’s no stretch to think that our adversaries, like China, would be happy to pounce given the opportunity.

Another way out of the deficit spending—ballooning federal debt morass is to tax our way out, or limit social safety net programs like social security and Medicare. Both parties have said, so far, that Social Security and Medicare cuts or benefit changes are off the table (we have written about this before)—and Republicans, and many moderate Democrats, will likely continue to reject tax increases. So, are we back where we started, kicking the debt-can down the road, hoping for the best and that no-one cares?

“Bipartisan neglect of the debt would be excusable if the underlying problem were somehow solving itself, but the opposite is true,” according to a Washington Post editorial. “The list of possible long-term negative consequences includes high interest rates, severe budget cuts and even a government default.” The Wall Street Journal’s Seib strikes a similar tone. “History,” he writes, “offers some cautionary notes about the consequences of swimming in debt. Over the centuries and across the globe, nations and empires that blithely piled up debt have, sooner or later, met unhappy ends.”

Personally, I prefer happy endings, and for far too long we’ve been giving Washington too much credit. “Giving money and power to politicians,” humorist Dave Barry once equipped “is like giving whiskey and car keys to a 16-year old.” Perhaps it’s time we took away the keys, the bottle, oh, and the credit card.